ETF Tracker StatSheet

You can view the latest version here.

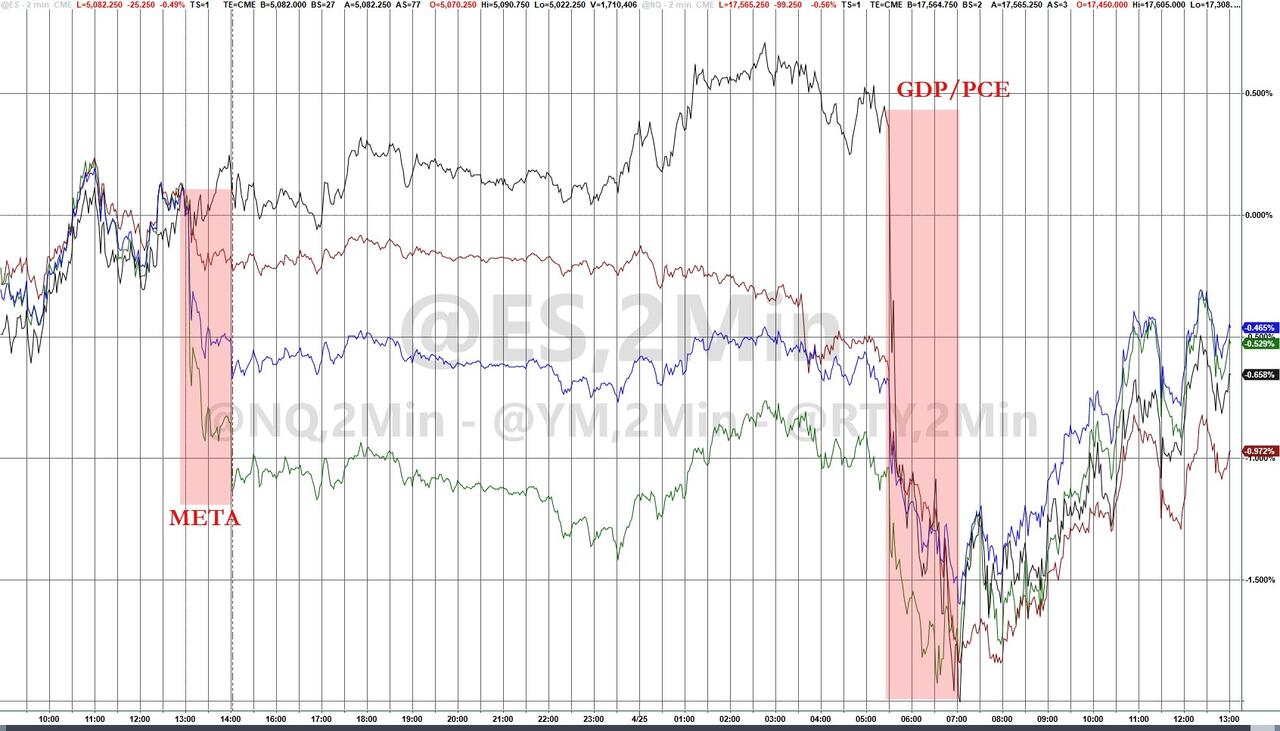

BIG TECH EARNINGS PROPEL STOCKS: ALPHABET AND MICROSOFT LEAD THE CHARGE

- Moving the markets

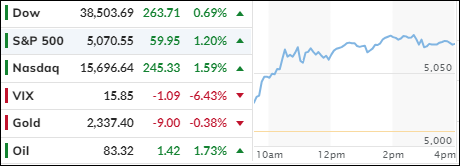

In today’s dynamic stock market, Big Tech giants Alphabet and Microsoft took center stage, fueled by robust earnings reports. Alphabet’s stock surged over 10%, marking its most impressive performance since July 2015. Meanwhile, Microsoft posted a solid 3% gain on the back of strong fiscal third-quarter results.

The positive sentiment extended beyond individual stocks. Investors found encouragement in March’s core personal consumption expenditures (excluding food and energy), which rose by 2.8% year-on-year—surpassing the expected 2.7%. Personal spending also exceeded estimates, growing by 0.8%.

These developments helped major stock indexes regain their footing after yesterday’s downturn. However, the blue-chip Dow faced headwinds, sliding 375 points due to concerns about economic slowdown and persistent inflation but scoring a modest gain today.

Traders remain optimistic, asserting that rate cuts are unnecessary for the bull market’s continuation. Instead, they anticipate sustained economic expansion and robust corporate profits—already evident among market giants—to propel stock prices to new highs.

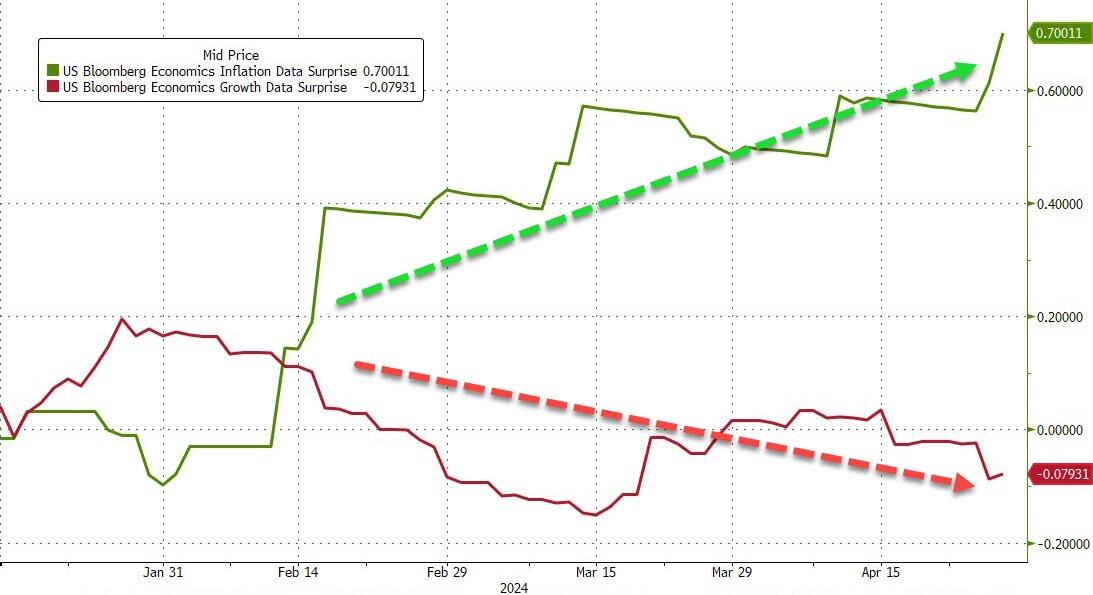

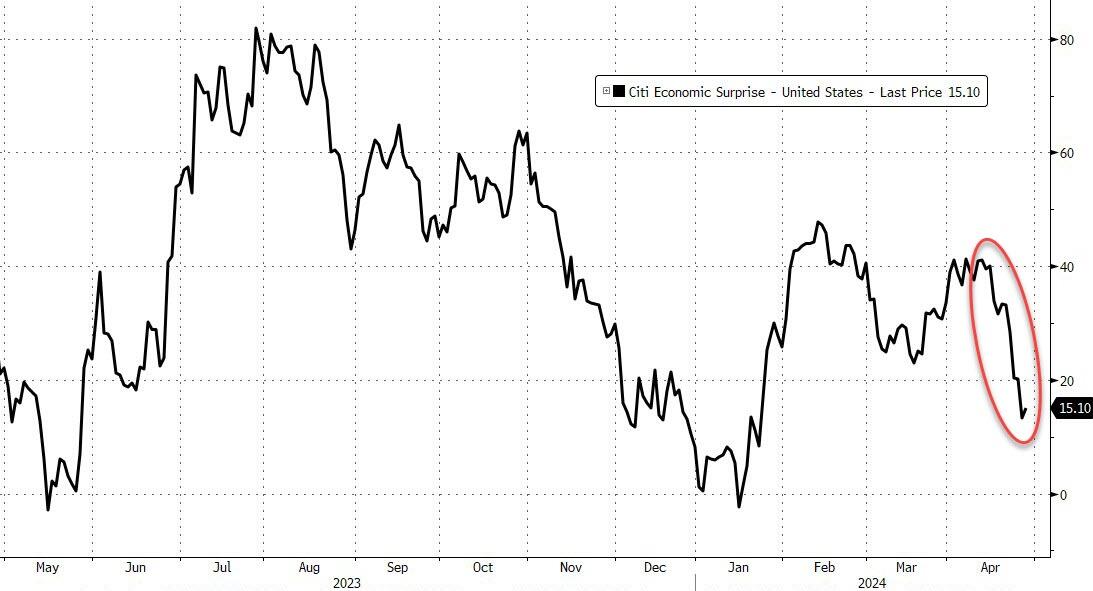

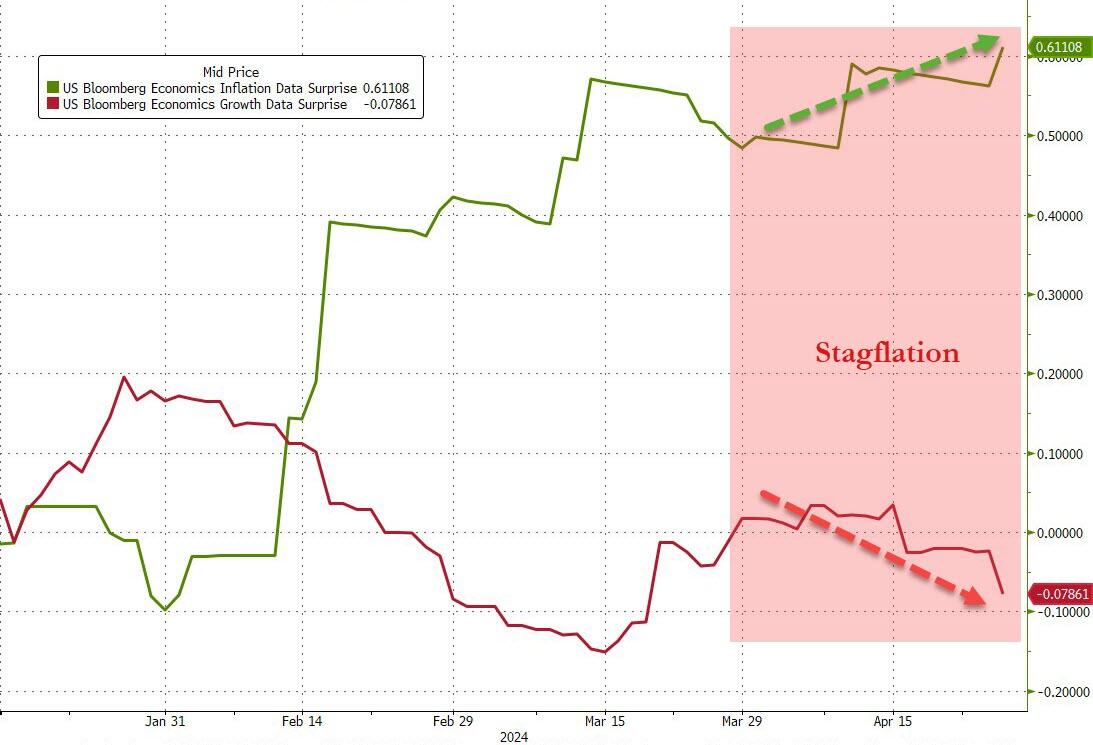

Remarkably, despite rising rates, higher inflation, and lower growth, stocks defied expectations. The combination of these factors painted a picture of stagflation, leading the Citi Economic Surprise index to deteriorate and rate-cut expectations to hit new cycle lows.

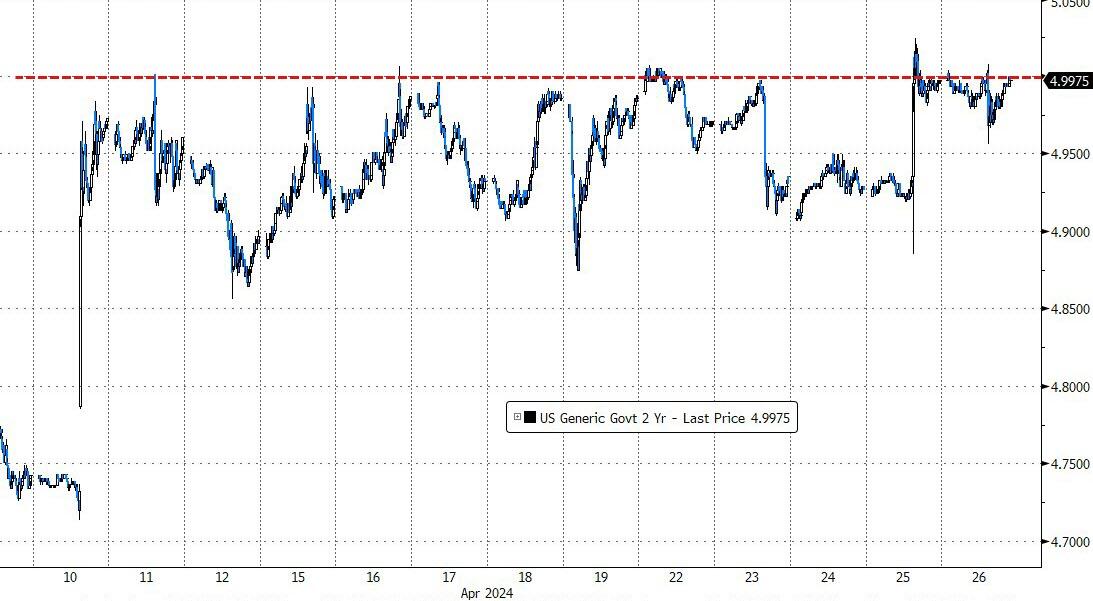

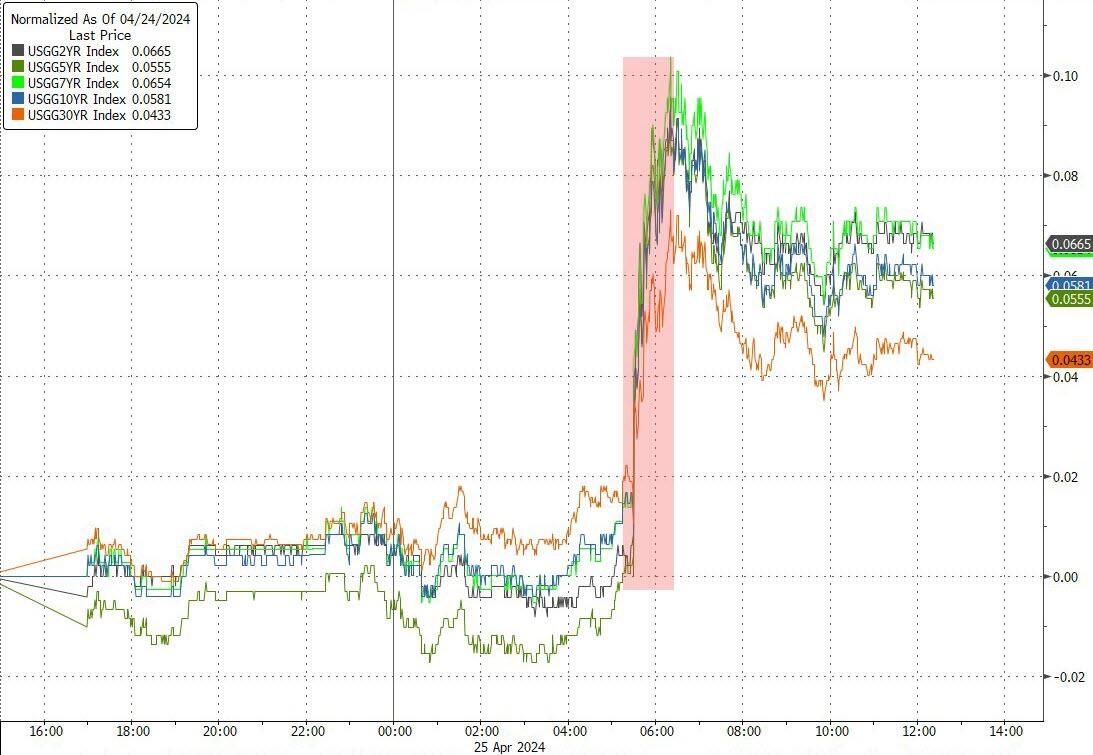

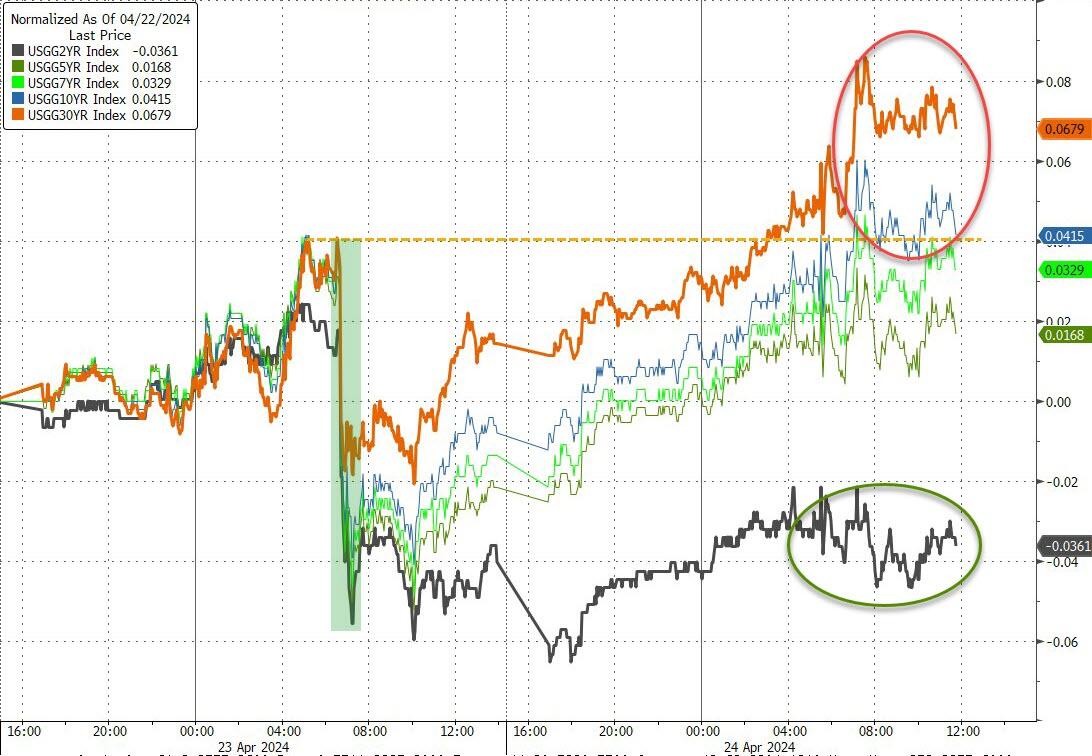

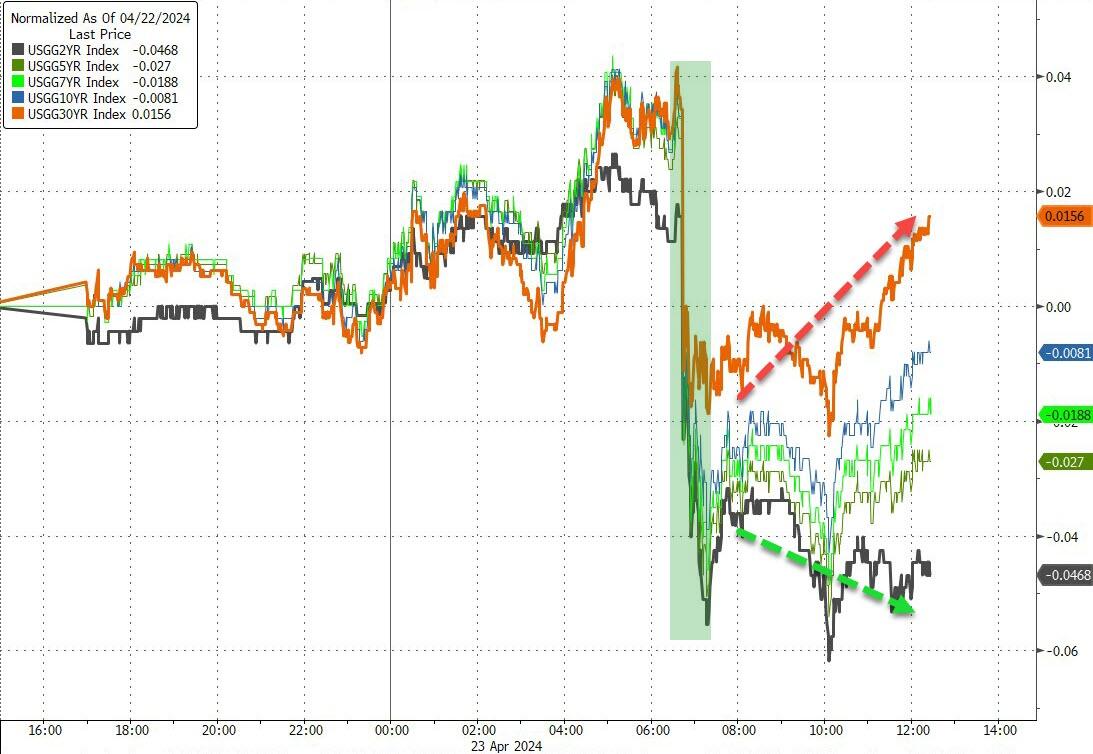

Bond yields surged across the board, with the 2-year yield still hovering around 5%. Interestingly, the Nasdaq outperformed, gaining 4%, while the Dow lagged.

The positive momentum received an additional boost from the most significant short squeeze since March’s first week. This propelled the MAG7 stocks up by over 5% this week, although META faced challenges and tanked. Notably, Tesla, Google, and Microsoft played a pivotal role in lifting the overall market sentiment.

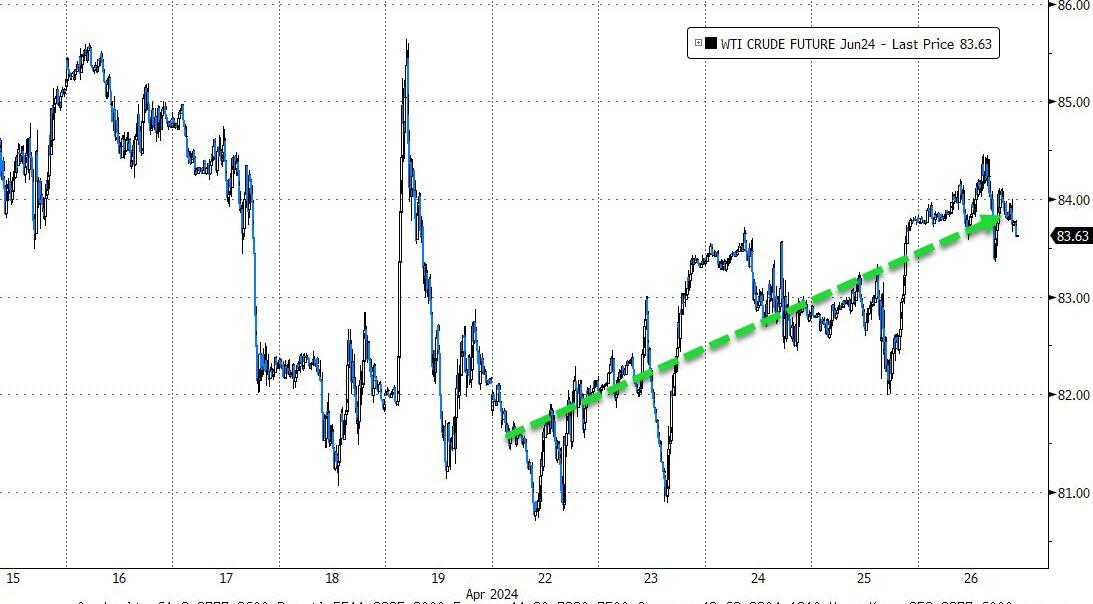

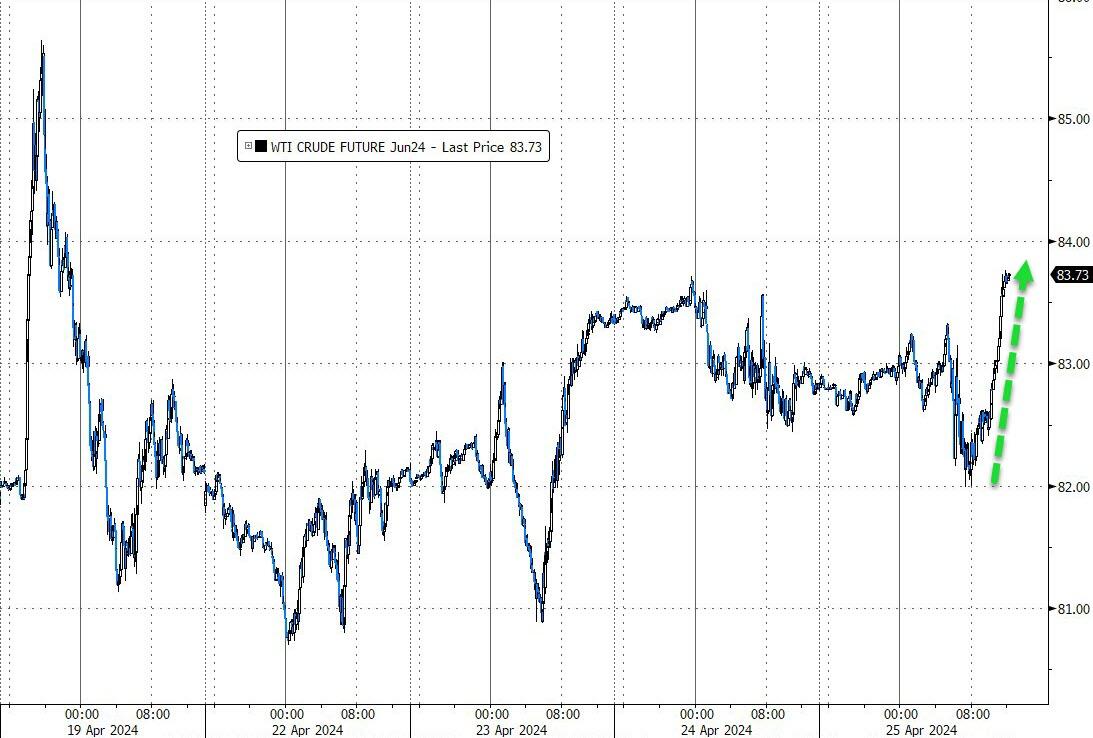

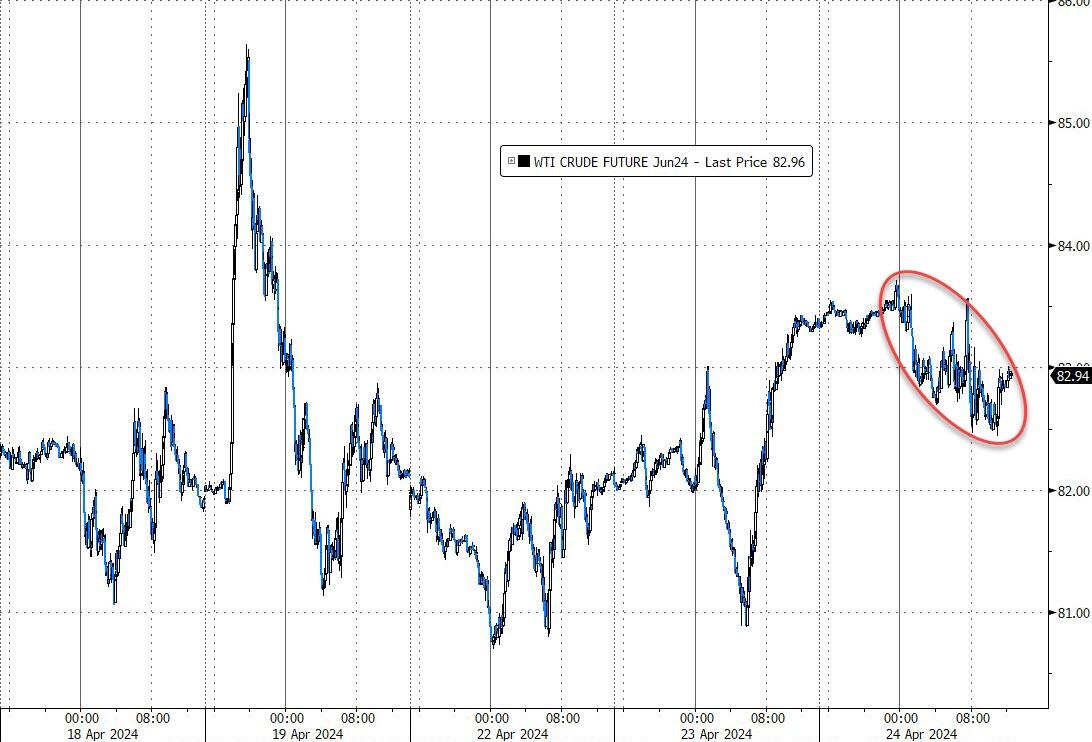

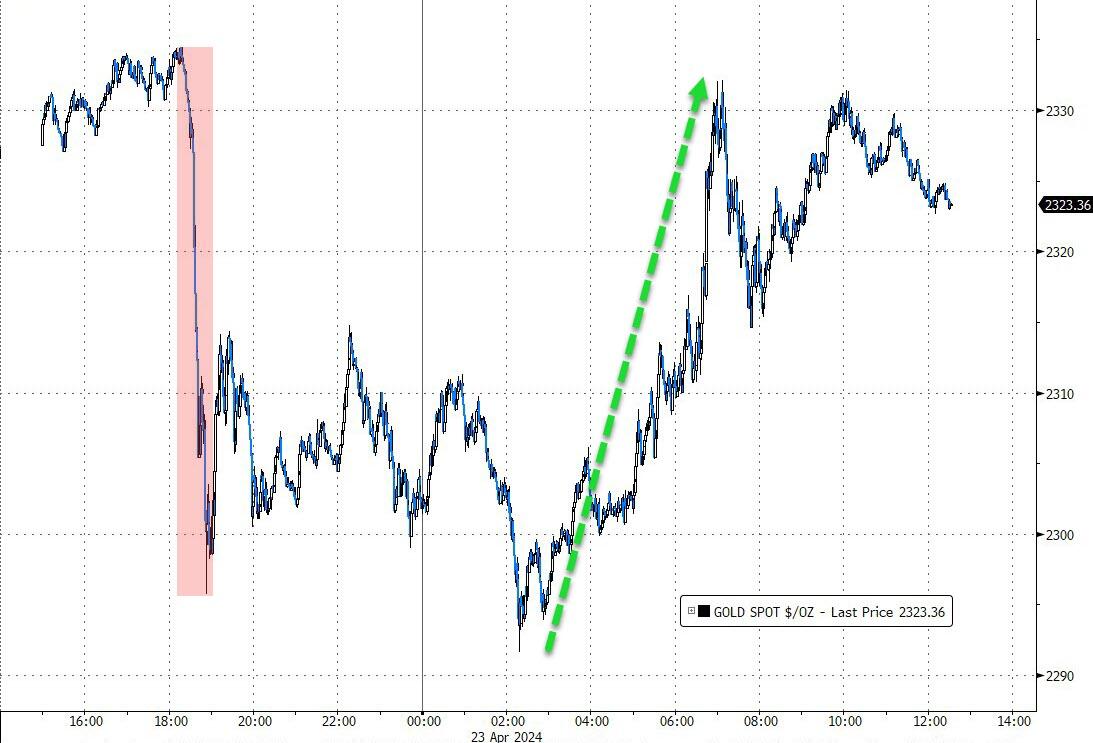

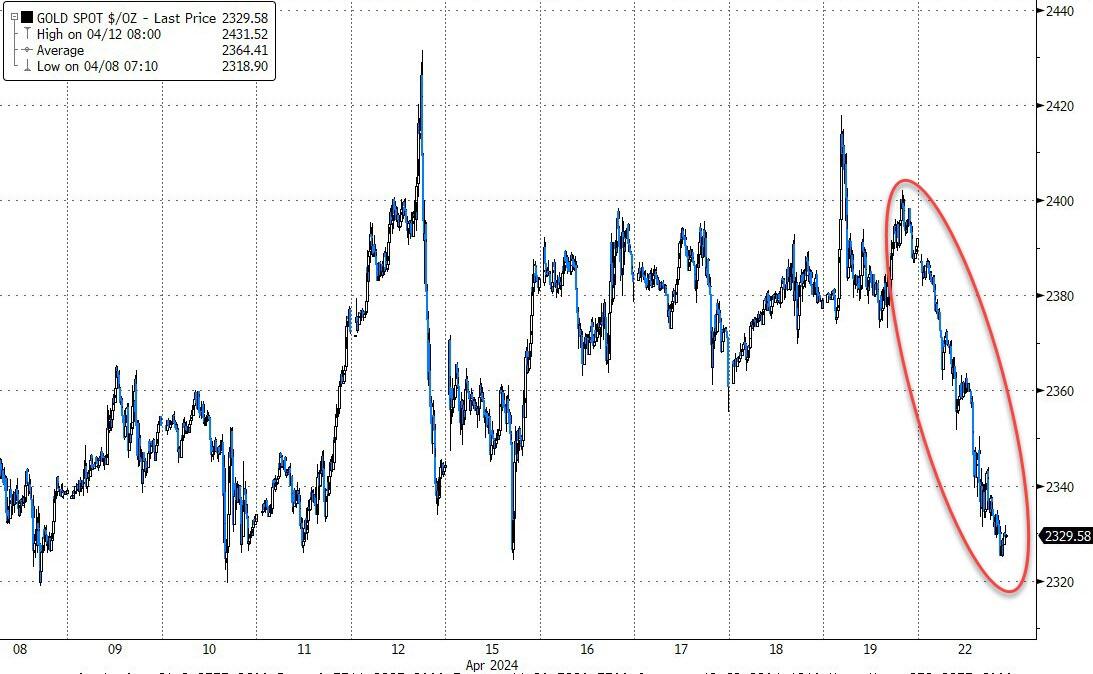

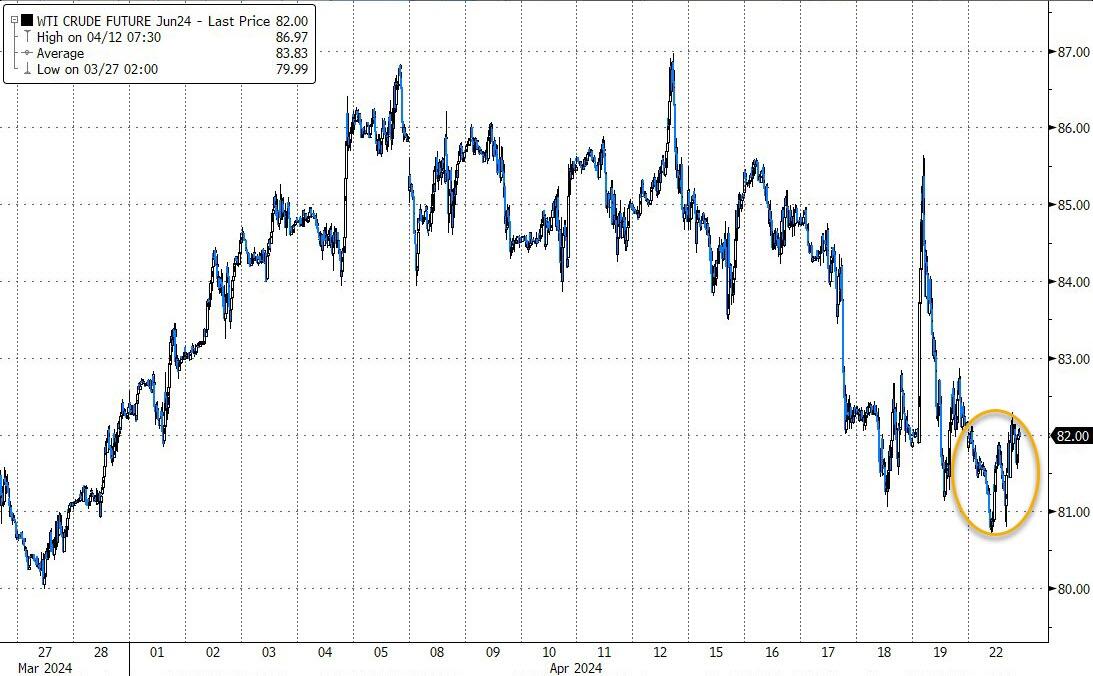

Despite the market’s wild gyrations, the dollar ended the week unchanged. Gold, although slipping, found support at the $2,300 level, while crude oil finally rallied after two weeks of decline.

However, heightened volatility in recent weeks leaves me pondering:

Can Powell’s upcoming FOMC meeting restore calmness to the markets?

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}